Oil prices are spiking above $100/barrel this morning as the Iran conflict continues with no near-term resolution currently in sight. This is up from less than $70/barrel when the attacks began on February 28. The S&P 500 has fallen roughly 3% over this time period and is now down roughly 2% year-to-date. Bond prices have also suffered, with the 10-year Treasury yield rising from roughly 3.96% to 4.15% as investors start to price in higher inflation from the spike in oil prices and further deficits from increased military spending.

Iran’s Significance to Markets:

Iran currently supplies roughly 5% each of global oil and natural gas production, and is a top five country for both in terms of proven reserves. Oil and natural gas make up 82% of Iran’s exports. China is its primary buyer of oil, while Turkey and Iraq are its primary buyers of natural gas. Even more importantly, Iran borders the Strait of Hormuz, the narrow waterway connecting the Persian Gulf to the Gulf of Oman. Commercial shipping through the Strait of Hormuz has ground to a near-standstill, impacting supplies not only from Iran but also Saudi Arabia, Bahrain, Kuwait, Iraq, Qatar, and the UAE. Overall, roughly 20% of global oil production and 20% of global liquified natural gas (LNG) production travel through the Strait of Hormuz. Oil is a true globalized commodity as it is easily shipped via tankers, and thus world oil prices are spiking more than US natural gas prices, which are more localized and primarily shipped via pipeline. However, some countries that are large importers of LNG are seeing their natural gas prices spike as well, such as China, Japan, South Korea, India, and the European Union. The Strait of Hormuz is also a major transportation artery for urea and ammonia, key ingredients in fertilizers.

Reasons to be Optimistic:

Most major countries have strong incentives for this conflict to end quickly:

- United States: According to a January 2026 Pew Research poll, inflation is still the top economic concern for the vast majority of Americans. The price of oil is a major component of inflation, not only for its direct impact on fuel prices, but also for its indirect impact via the cost of shipping/trucking. With the midterm elections coming in November, the administration should be highly motivated to lower oil prices.

- China: Roughly 40% of China’s oil consumption comes from Middle East sources. Like the US, China has a strategic crude oil stockpile, but an extended closure of the Strait of Hormuz would be highly problematic and should incentivize China to lean on its strategic partner Iran to end the conflict.

- India: Over 40% of India’s oil consumption comes from Middle East sources. India recently struck a trade agreement with the United States that required them to lower their reliance on Russian oil, and its strategic reserve is estimated at less than half of China’s, making India even more reliant on an operational Strait of Hormuz.

- European Union (EU): Beyond the inflation risk caused by the spike in crude oil prices, the EU is now exposed to global LNG prices given it has been trying to reduce its reliance on Russian natural gas pipelines. The EU also fears that the spike in oil prices could give Russia more power to continue the war in Ukraine.

- Japan: Japan imports 95% of its oil and almost 100% of its natural gas via LNG. The country has a large strategic oil reserve, but it will be highly exposed to the spike in oil and LNG prices if the conflict continues.

- The Gulf States (Saudi Arabia, Qatar, UAE, etc.): Not only is the current conflict impacting these countries’ ability to export their oil and LNG, it is also harming their reputation as international business hubs. Examples include recent strikes against Dubai International Airport, which had become the world’s busiest airport for international passenger traffic, and Amazon Web Services datacenters in the UAE and Bahrain.

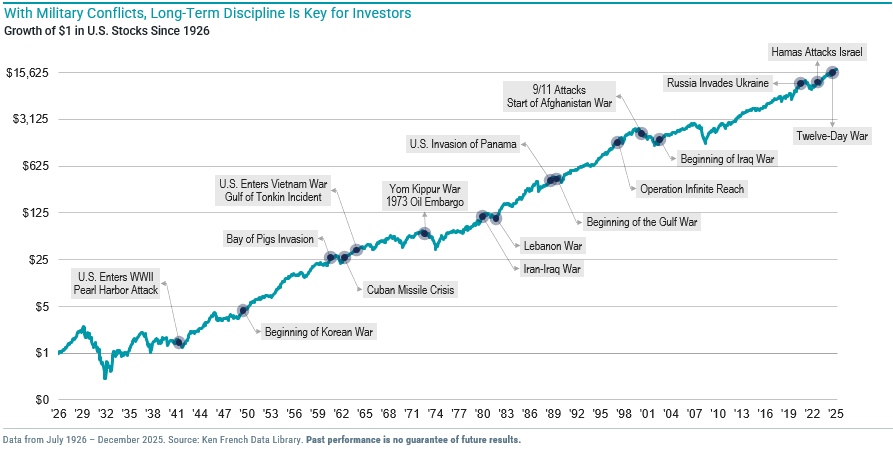

While military conflicts have historically caused higher short-term volatility, the start of a new conflict has never been a reason to sell for long-term investors. Examining the conflicts from the chart below, US stocks were higher three months later 69% of the time and higher three years later 100% of the time, with similar results for international equities.

Reasons to be Cautious:

- Despite the deaths of many leaders, the overall hardline leadership in Iran still appears to be firmly entrenched. This means that the US and Israel may need to escalate their attacks even further or abandon some of their strategic objectives like regime change.

- The stock prices of Technology companies, which dominate the S&P 500, may be disproportionately impacted by rising interest rates. Their high growth rates mean that their largest projected cash flows are far in the future, making them more sensitive to the discount rate used in a present value analysis. Conversely, Energy companies that could benefit from higher oil prices make up under 4% of the S&P 500.

- The longer the Strait of Hormuz is closed, the worse things become because (1) global inventories and stockpiles get depleted and supplies of oil/LNG/urea become truly constrained; (2) the storage facilities of the Gulf States become full causing them to actually halt oil/gas production, a process that can take weeks to reverse, (3) the reputation of the Gulf States as reliable trade/business partners gets worse the longer the conflict persists, depending on how it is ultimately resolved.

GGS Thoughts:

When we look at similar historical events as a guide, there is a clear lesson that staying invested at your target risk level and not attempting to time the market is the best course of action for long-term investment success. We understand that this can be difficult when the headlines sound dire and volatility in the market has spiked, but we remain optimistic given the aligned incentives of the world’s major powers to find a resolution. We will continue to monitor the latest Iran conflict developments and will make the adjustments we deem appropriate to client portfolios.

Footnotes:

- https://www.iea.org/world/natural-gas

- https://www.eia.gov/tools/faqs/faq.php?id=709&t=6

- https://worldpopulationreview.com/country-rankings/oil-reserves-by-country

- https://worldpopulationreview.com/country-rankings/natural-gas-by-country

- https://www.statista.com/statistics/294379/iran-main-export-partners/

- https://tradingeconomics.com/iran/exports#:~:text=Oil%20and%20natural%20gas%20are,fruits%2C%20ceramic%20products%20and%20metals.

- https://www.statista.com/statistics/1127284/iran-volume-of-natural-gas-pipeline-exports/

- https://www.pewresearch.org/politics/2026/02/04/a-year-into-trumps-second-term-americans-views-of-the-economy-remain-negative/

- https://realeconomy.rsmus.com/market-minute-chinas-dependence-on-middle-eastern-oil/#:~:text=Before%20the%20war%2C%20China%20is,the%20rising%20price%20of%20oil

- Avantis Investors ETF Field Guide February 2026

- https://www.reuters.com/sustainability/boards-policy-regulation/japans-middle-east-energy-dependency-how-it-mitigates-shocks-2026-03-04/