Since March 2020, the global economy has undergone multiple dramatic changes driven primarily by adaptations of businesses, consumers, employees, and governments to the COVID-19 pandemic. Some examples:

- Severe lockdowns followed by staggered reopening policies

- Massive government stimulus followed by fiscal and monetary tightening

- Huge demand increases for consumer goods and supply chain gridlock followed by the current “freight recession” 1

- Collapse in travel followed by significant recovery 2

- Worries about deflation followed by the highest inflation rate since 1980 3

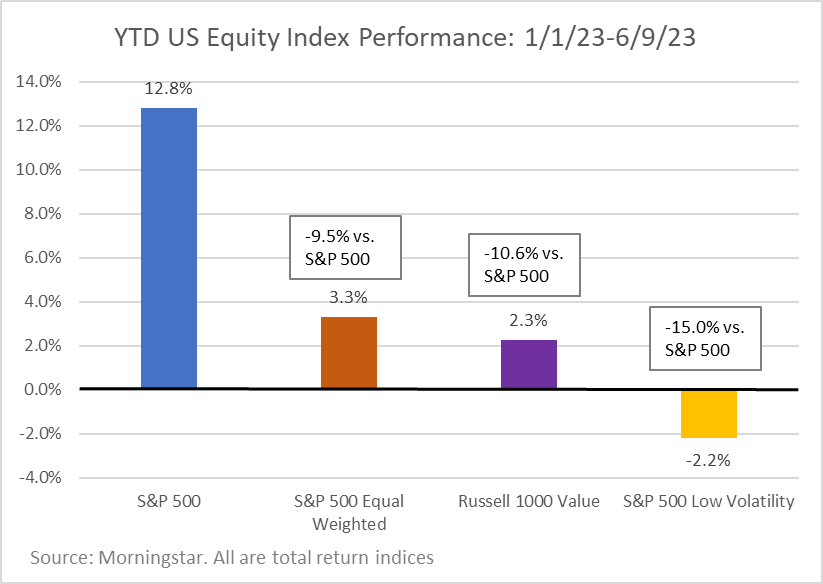

The shifting economic backdrop continues to this day and has led to distortions in economic data, with some metrics showing a US economy currently in recession while others show continued healthy growth.4 This unusual economic environment has also led to significant stock price performance dispersion between industries and companies.5 Looking at the S&P 500 year-to-date (YTD), just 10 of the 500 stocks in the index have driven 90% of the gains (Alphabet, Amazon, AMD, Apple, Broadcom, Meta, Microsoft, NVIDIA, Salesforce, Tesla).6 These companies, all of which could be considered Technology stocks, carry a high weight in the index and not owning them in the requisite size has led to relative underperformance for many active managers.7

In fact, we are currently experiencing the largest YTD underperformance on record for the S&P 500 Equal Weighted TR Index relative to the market cap-weighted S&P 500 TR Index.8 Similarly, there has been abnormal YTD underperformance of lower-priced value stocks and more defensive, low-volatility stocks, both of which are factors we favor in our individual stock selection as they have historically led to risk-adjusted outperformance.9

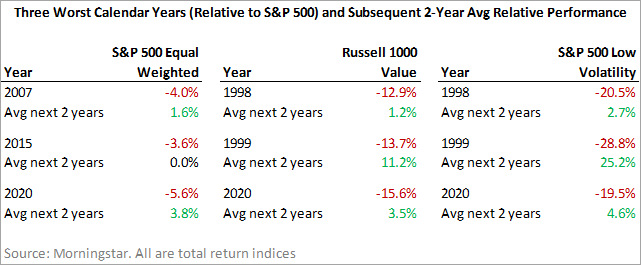

Looking at the history of these indices relative to the S&P 500, the only larger calendar year percentage gaps (positive or negative) have occurred during extreme market years such as the 1998-2001 Tech Bubble, the 2008-2009 Great Financial Crisis, and the 2020 COVID-19 Pandemic.10 Importantly, these three indices have all historically rebounded after periods of severe underperformance: 11

Bottom line, this has been an unusual start to the year for the US stock market. When extreme relative performance gaps between US equity market indices do occur, they often appear to be the “new normal.” Yet, history shows that they tend to reverse over subsequent years as the underlying economic situation shifts or as overly optimistic/pessimistic forecasts and valuations fail to be realized. Therefore, we believe it is critical to stick to our core investment strategy during years like 2023 even as it is tempting to make significant changes and chase the types of companies currently in favor. We continue to believe that our disciplined process of owning high-quality companies trading at attractive valuations is the best strategy to help clients succeed in their long-term investing goals.